Why Do "Stablecoins" Make Traditional Finance Anxious?

- Dr Colin Lee

- Apr 23

- 3 min read

A core contradiction in Hong Kong’s current financial transformation is that while regulation has moved forward, perception remains stuck in the past.

I will help you break down the entire logic and supplement a few key points to make the discussion more multi-dimensional.

I. What exactly is a stablecoin?

To put it in a single sentence:A stablecoin is a "blockchain-native digital cash carrier."

It is not inherently a speculative tool, but rather a payment and settlement technological architecture.

The problem is that there are three completely different types of "stablecoins" in the market, yet they are often conflated.

II. Three types of stablecoins, fundamentally different

1️⃣ Algorithmic stablecoins (High-risk experimental products)

Not necessarily backed by real assets

Rely on algorithmic mechanisms to maintain price pegs

Typical failure case: Terra/Luna (collapsed in May 2022)

This category is indeed extremely risky and has cast a psychological shadow over traditional finance.

2️⃣ Overseas-issued fiat-reserve stablecoins (e.g., USDT, USDC)

Characteristics:

Claim to have 1:1 reserves

Issued by private companies

Regulatory frameworks vary greatly depending on the jurisdiction

Reserve transparency and legal protection levels vary

They are already the primary settlement medium in the global crypto market, but regulatory standards are not uniform.

3️⃣ Hong Kong's "Compliant Stablecoins" (Regulatory type)

According to the Hong Kong Monetary Authority's (HKMA) institutional design, its core requirements include:

✅ 1:1 high-quality reserve assets

✅ Independent custody of reserves

✅ Regular audits

✅ Statutory redemption rights

✅ Issuers must be licensed

The essence of this design is:

Embedding blockchain payment technology into the traditional financial regulatory framework.

It is not a decentralized utopia, but a "regulated blockchain payment tool."

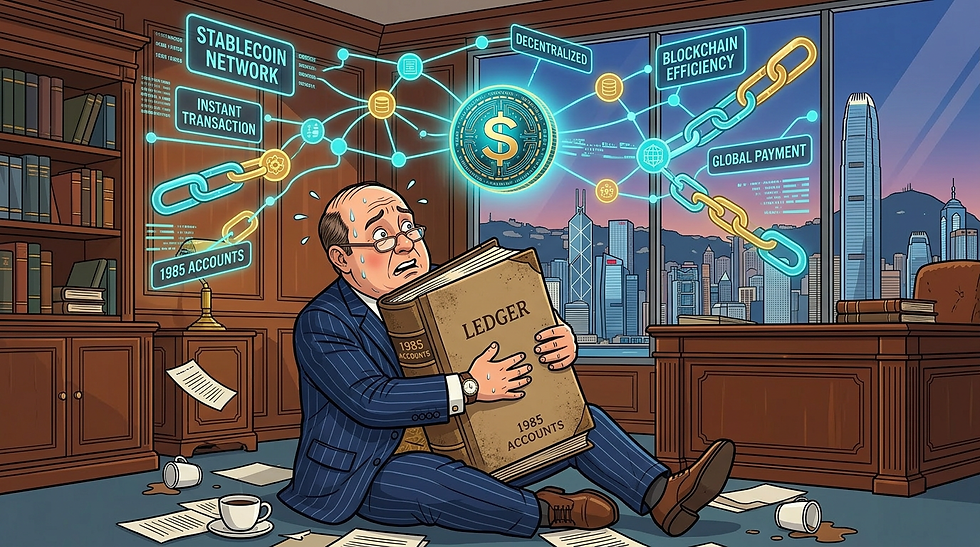

III. Why is traditional finance anxious?

Because it touches upon three core interest structures:

1️⃣ Clearing and Settlement Revenue

Cross-border payment chains are long and fees are high, making them a significant source of revenue for banks.

If stablecoins can achieve T+0 atomic settlement, it equates to compressing the intermediary layers.

2️⃣ Deposit Stability

If enterprises can hold:

Hong Kong dollar stablecoins

US dollar stablecoins

Do they still need to maintain large amounts of demand deposits in banks?

This is the true structural anxiety for banks.

3️⃣ Sense of Financial Control

In the traditional system, the ledger resides with the bank.

In blockchain, the ledger is on a distributed network.

This change in the control structure brings a greater psychological impact than a technological one.

IV. Stablecoins ≠ Tokenized Deposits

Many people confuse this point.

Comparison Item | Stablecoins | Tokenized Deposits |

Issuer | Specialized issuing institutions | Commercial banks |

Legal Relationship | Claim against the issuer | Claim against bank deposits |

Reserve Format | Independent reserve assets | Bank balance sheet |

Risk Structure | Reserve risk | Bank credit risk |

Tokenized deposits are merely a "digital encapsulation of bank deposits."

Stablecoins, on the other hand, are more like a "digital form of a money market fund + payment interface."

V. Is it a revolution or an upgrade?

I would say quite objectively:It is not a disruption.

It is an upgrade of the payment layer.

Just like:

Email did not disrupt banks

But it disrupted the fax machine

Stablecoins change the "settlement layer," not the "credit creation layer."

VI. Three issues truly worth paying attention to

Even if one supports stablecoins, these cannot be ignored:

1️⃣ Bank Run Risk

If market panic occurs, will large-scale redemptions cause liquidity pressure?

2️⃣ Systemic Concentration Risk

What if one or two stablecoin issuers monopolize the market?

3️⃣ Monetary Policy Transmission

If massive amounts of funds are converted into stablecoins, will it affect the liquidity of the banking system?

These are the issues that regulators truly care about.

VII. The Reality in 2026

Stablecoins are no longer a gray-area topic in Hong Kong.

They have become:

Enterprise fund management tools

A component of Web3 infrastructure

Cross-border trade settlement pilots

Supply chain finance testing grounds

But whether they will become a "mainstream payment infrastructure" depends on:

Whether banks are willing to cooperate

Whether enterprises will truly adopt them

Whether regulation remains flexible

A Pragmatic Conclusion

Stablecoins are not a scourge.But they are not saviors either.

They are an efficiency tool.

What truly determines their success or failure is not the technology itself, but:Whether the financial system is willing to restructure its processes.

If Hong Kong can find a balance between regulation, security, and efficiency, it may truly become the model for the next upgrade in financial infrastructure.

[Limited-Time Expert Consultation Invitation]

FOFA sincerely invites visionary entrepreneurs and investors to engage in deep, practical exchanges regarding the aforementioned trends—specifically the implementation of "AI Agent Labor Systems (Agentic AI)."

We will provide you with a complimentary expert planning consultation to help you tailor a specific entrepreneurial path or investment blueprint, allowing technology leverage to serve your asset appreciation.

Book your strategic dialogue NOW:

![[Revealed] The Richest Fed Chair in History? Kevin Warsh’s 69-Page Financial Disclosure Exposed: Uncovering a Billion-Dollar Dynasty and Tech Startup Investment Empire](https://static.wixstatic.com/media/71b74c_0ad16886245f48d1b77a56e47c5f2795~mv2.png/v1/fill/w_980,h_547,al_c,q_90,usm_0.66_1.00_0.01,enc_avif,quality_auto/71b74c_0ad16886245f48d1b77a56e47c5f2795~mv2.png)

Comments